Impairment Expense Journal Entry - Simplified approach applicable to certain trade receivables, contract assets and lease receivables. An impaired asset is an asset valued at less than book value or net carrying value. What is an impaired asset? Ifrs 16 finance lease example (lessee) amortization schedule. The following journal entry must be recorded to account for this condition: The journal entry is debiting impairment expense and credit the impaired asset. Then records the impairment loss. Web international accounting standard 36 impairment of assets (as revised in 2004) was approved for issue by eleven of the fourteen members of the international accounting standards board. Messrs cope and leisenring and professor whittington dissented. The system creates a journal entry that debits the impairment expense posting account and credits the lease asset posting account.

Journal Entries Archives Double Entry Bookkeeping

The other side of the journal entry will impact the expense on income statement. Web ias 36 impairment of assets seeks to ensure that an.

Examples of How to Record a Journal Entry for Expenses Hourly, Inc.

Although a separate accumulated impairment loss account has been credited here, it is common in practice to simply credit accumulated depreciation. The journal entry to.

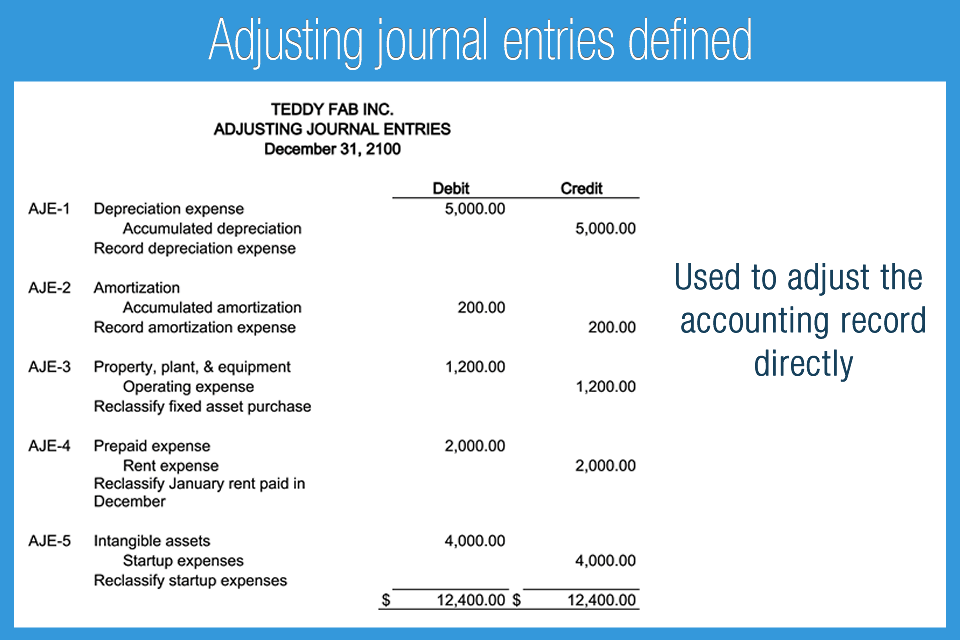

Adjusting Journal Entries Defined Accounting Play

If the carrying amount exceeds the recoverable amount, the asset is described as impaired. What is an impaired asset? Web three approaches to impairment. This.

Accounting For Intangible Assets Complete Guide for 2023

Ifrs 16 finance lease example (lessee) amortization schedule. Dr impairment write down (expense) If the carrying amount exceeds the recoverable amount, the asset is described.

ons Presented below is information related to equipment owned by Swifty

If due to any event the impaired asset regains its value, the gain is first recorded in income statement to the extent of original impairment.

Accounting for Impairments of PPE YouTube

However, before recording the impairment loss, a company must first determine the recoverable value of the asset. Decides in october of year 1 to dispose.

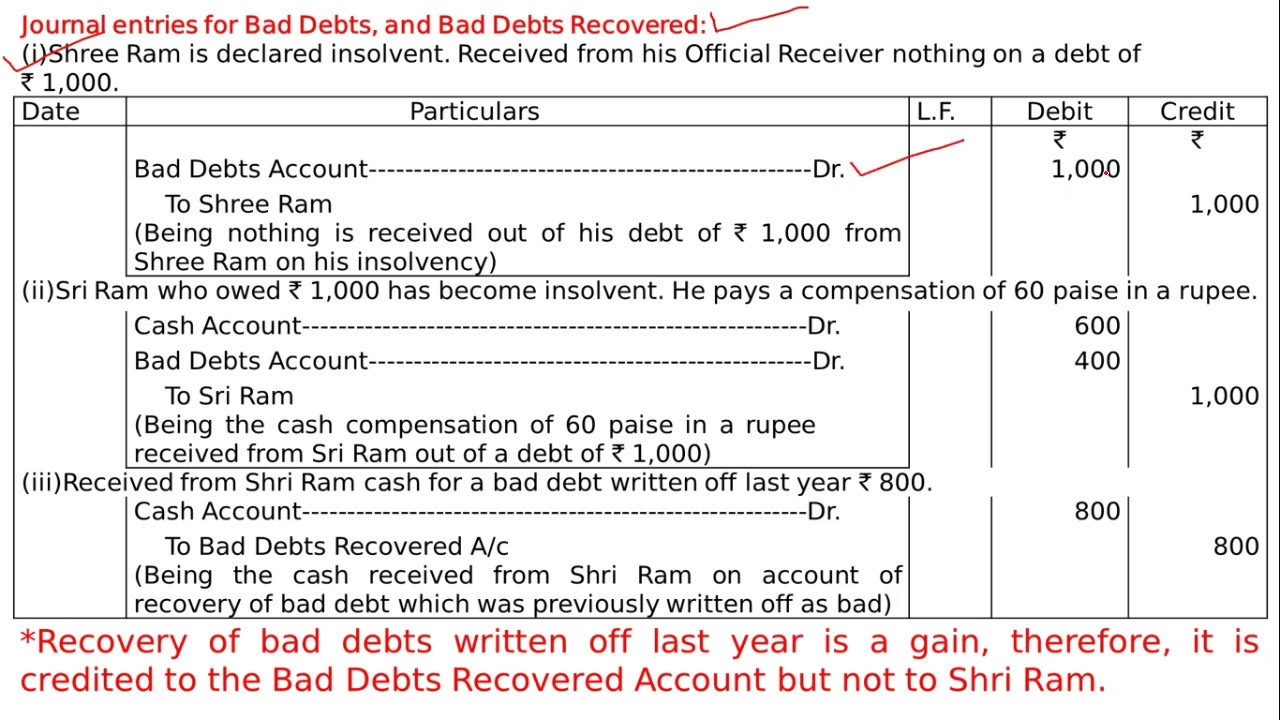

Journal Entries for Bad Debts and Bad Debts Recovered YouTube

In other words, an impaired asset has a current market value that is less than the value listed on the balance sheet. Ias 36 also.

The New Guidance for Goodwill Impairment The CPA Journal

Web the impairment loss is when the book value is higher than the fair value. As the result, company needs to reduce the asset’s book.

Allowance For Impairment Of Trade Receivables UnBrick.ID

The higher of fair value less costs of disposal and value in use). Web the core principle in ias 36 is that an asset must.

Impairment Loss Journal Entry BronsonaresTownsend

Web ias 36 impairment of assets seeks to ensure that an entity's assets are not carried at more than their recoverable amount (i.e. The group’s.

Simplified Approach Applicable To Certain Trade Receivables, Contract Assets And Lease Receivables.

If the carrying amount exceeds the recoverable amount, the asset is described as impaired. This loss will be as below. An impaired asset is an asset valued at less than book value or net carrying value. Web the core principle in ias 36 is that an asset must not be carried in the financial statements at more than the highest amount to be recovered through its use or sale.

What Is Considered A Lease Under Ifrs 16?

Dr impairment write down (expense) Based on management’s best estimate of net cash flow projections (after the 40% cut). Their dissenting opinions are set out after the basis for conclusions. As the result, company needs to reduce the asset’s book value from the balance sheet.

Decides In October Of Year 1 To Dispose Of An Asset Group That Is A Component Of An Entity.

Ias 36 also outlines the situations in which a company can reverse an impairment loss. Web the journal entry would be: The higher of fair value less costs of disposal and value in use). Web three approaches to impairment.

The Recoverable Amount Of An Asset Or A Cgu Is The Higher Of Its Fair Value Less Costs To Sell And Its Value In Use.

The following journal entry must be recorded to account for this condition: The present value factor is calculated as k = 1/ (1+a) n, where a = discount rate and n = period of discount. Calculation of the value in use of the country a cash‑generating unit at the beginning of 20x2. Web ias 36 impairment of assets seeks to ensure that an entity's assets are not carried at more than their recoverable amount (i.e.