Cecl Journal Entries - Us loans & investments guide. Home » current expected credit losses (cecl): Even before its official publication in 2016, the financial accounting standards board (fasb) standard asc 326, better known as current expected credit losses (cecl), has been a topic of great discussion and debate. Implicit in that calculation is the 99.5% probability that there is no default. Web the financial accounting standard board’s (fasb) recently issued current expected credit loss (cecl) model attempts to align measurement of credit losses for all financial assets held at amortized cost, and specifically calls out potential improvements to the accounting for purchased credit impaired (pci) assets. Reduce the complexity in us gaap by decreasing the number of credit impairment models that entities use to account for debt instruments. The standard is effective for most sec filers in fiscal years and interim periods beginning after december 15, 2019, and for all others it takes effect in fiscal years beginning after december 15, 2022. Web the following table compares the amounts reported by the institution in its call reports for december 31, 2021, and march 31, 2022, as a basis for illustrating the journal entries the institution would make to reflect the effects of adopting the new credit losses standard as of january 1, 2022, and applying it during the first quarter of 2022. In practice, there are two main approaches to determine ecls (expected credit losses): Web the objectives of the cecl model are to:

The Impact of Assumptions on the CECL Estimate The CPA Journal

The federal reserve board (frb) has updated reporting requirements to address cecl and broader credit loss requirement changes. Home » current expected credit losses (cecl):.

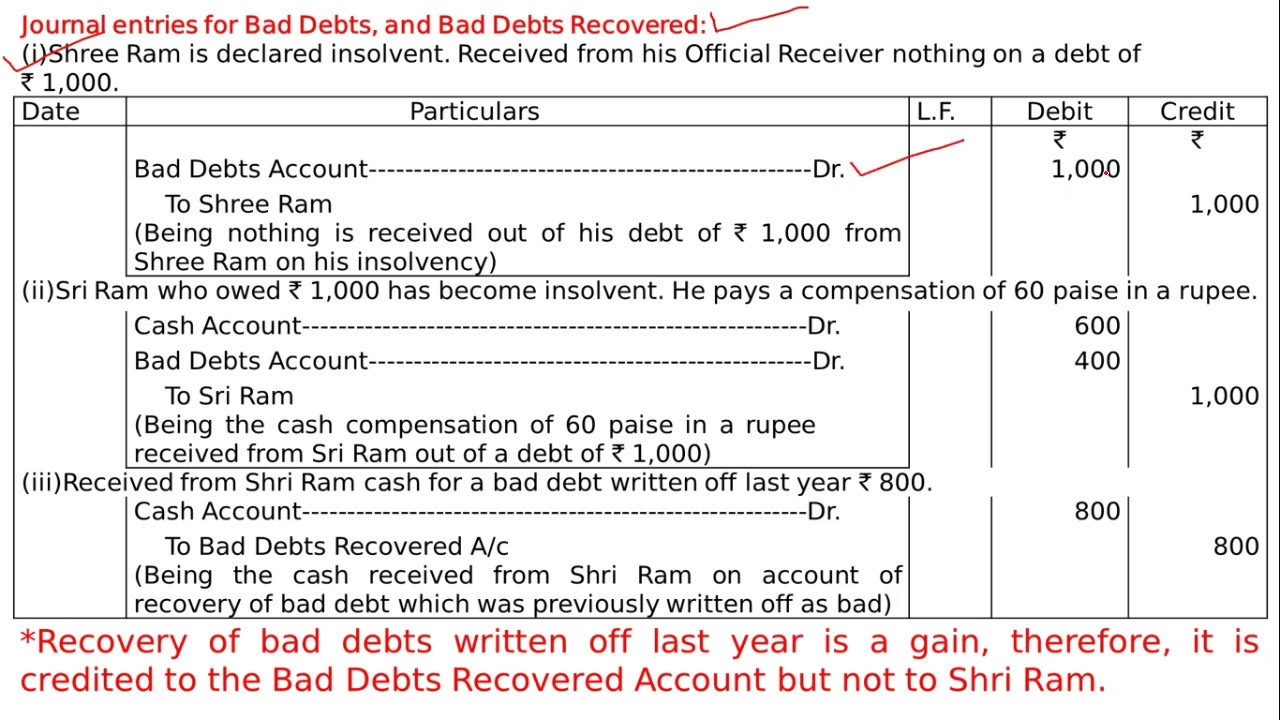

Bad Debts Recovered Journal Entry CodyaxBray

The design, documentation, and validation of expected credit loss estimation. Cecl was created to estimate expected credit loss on a loan or investment. Web the.

FASB unanimously approves CECL delay for most lenders Credit Union

Home » current expected credit losses (cecl): Eliminate the barrier to timely recognition of credit losses by using an expected loss model instead of an.

Allowance for Loan and Lease Losses CECL Deloitte US

Allowance matrix based on an entity's internal, historical credit loss data and past due receivables. Implicit in that calculation is the 99.5% probability that there.

![CECL and ASC 31030 [White Paper] Wilary Winn LLC](https://wilwinn.com/wp-content/uploads/CECL-ASC_-_3-768x689.png)

CECL and ASC 31030 [White Paper] Wilary Winn LLC

Web ifrs 9 does not provide any specifications on the design of the model. In practice, there are two main approaches to determine ecls (expected.

The Impact of Assumptions on the CECL Estimate The CPA Journal

Us loans & investments guide. Reduce the complexity in us gaap by decreasing the number of credit impairment models that entities use to account for.

Current Expected Credit Loss (CECL) Implementation Insights Deloitte US

Us loans & investments guide. Cecl was created to estimate expected credit loss on a loan or investment. Even before its official publication in 2016,.

CECL Model for Measurement of Credit Losses Windes

Web cecl implementation requires a multiphase process that includes assessment of the assets impacted, obtaining and evaluating data, assessing needed management review and governance controls,.

Making the Business Case for the CECL Approach Part II [White Paper

The federal reserve board (frb) has updated reporting requirements to address cecl and broader credit loss requirement changes. Web the financial accounting standard board’s (fasb).

journal entry format accounting accounting journal entry template

Eliminate the barrier to timely recognition of credit losses by using an expected loss model instead of an incurred loss model. Web the objectives of.

Even Before Its Official Publication In 2016, The Financial Accounting Standards Board (Fasb) Standard Asc 326, Better Known As Current Expected Credit Losses (Cecl), Has Been A Topic Of Great Discussion And Debate.

Web cecl implementation requires a multiphase process that includes assessment of the assets impacted, obtaining and evaluating data, assessing needed management review and governance controls, implementing the transition on day one, and then accounting and reporting going forward. The federal reserve board (frb) has updated reporting requirements to address cecl and broader credit loss requirement changes. Web the objectives of the cecl model are to: Regulatory reporting report forms change by the end of 2019.

Reduce The Complexity In Us Gaap By Decreasing The Number Of Credit Impairment Models That Entities Use To Account For Debt Instruments.

The design, documentation, and validation of expected credit loss estimation. The standard is effective for most sec filers in fiscal years and interim periods beginning after december 15, 2019, and for all others it takes effect in fiscal years beginning after december 15, 2022. Web the following table compares the amounts reported by the institution in its call reports for december 31, 2021, and march 31, 2022, as a basis for illustrating the journal entries the institution would make to reflect the effects of adopting the new credit losses standard as of january 1, 2022, and applying it during the first quarter of 2022. Web the implementation of cecl estimates has happened at a time when the auditing standards regarding estimates have been enhanced by the pcaob’s issuance of auditing standard (as) 2501, auditing accounting estimates, including fair value measurements (effective for audits of financial statements ending on or after december.

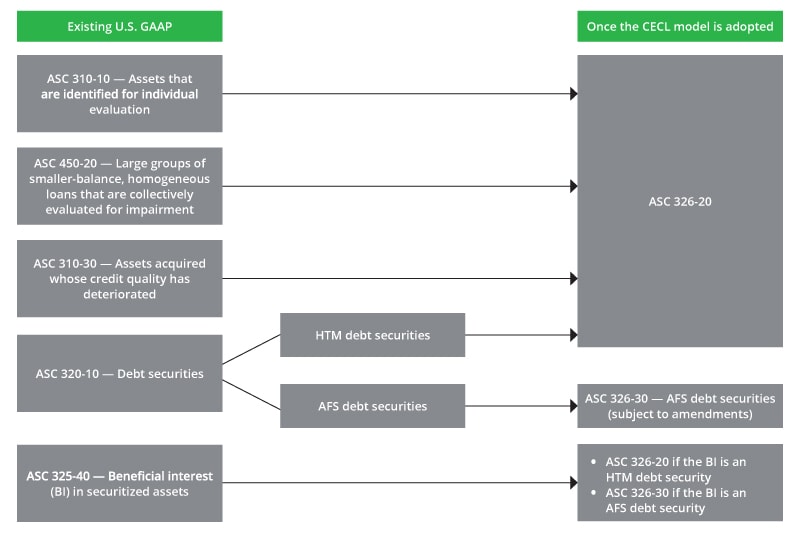

Web The New Accounting Standard Introduces The Current Expected Credit Losses Methodology (Cecl) For Estimating Allowances For Credit Losses.

Web example january 1, 2023 journal entry; Acl loans and leases (as0048) n/a: Web ifrs 9 does not provide any specifications on the design of the model. Web the financial accounting standard board’s (fasb) recently issued current expected credit loss (cecl) model attempts to align measurement of credit losses for all financial assets held at amortized cost, and specifically calls out potential improvements to the accounting for purchased credit impaired (pci) assets.

Us Loans & Investments Guide.

Web cecl becomes effective for federally insured credit unions for financial reporting years beginning after december 15, 2022. Volatility changes based on methods and models. Implicit in that calculation is the 99.5% probability that there is no default. The new standard is expected.